Initial reaction from our team of experts following today’s Spring Budget

Nimesh Shah – Chief Executive Officer

Abolishing the remittance basis for non-doms is expected to see large inflows of overseas monies into the UK for investment.

Introduction of the British ISA could give someone up to £26k in ISA savings per annum if they are also eligible for the Lifetime ISA. I question whether we need another form of ISA – wouldn’t it have been easier to increase the £20k ISA allowance which has remained stuck at this level since 2017/18.

If you’re a family of four, you could theoretically save £70k per annum across your ISAs – stocks and shares ISA + Lifetime ISA + British ISA + Junior ISA.

A surprising measure to increase the VAT registration threshold by £5k to £90k, but it doesn’t address the current cliff-edge problem with VAT for small businesses.

Losing the furnished holiday lettings regime is a welcome simplification – the regime had been significantly scaled back anyway. I’m surprised that it would cost anywhere close to £300m.

I completely agree that domicile is an archaic way to assess someone’s taxation basis – why should your father’s origin determine your UK personal tax status?

Capital Gains Tax (CGT): A new 24% CGT rate! This isn’t simplification. I count five CGT rates in play now: 0%/10%/20%/24%/28%.

Child Benefit Charge: Very welcome measure to reform the horrible high income child benefit charge – increasing the threshold to £60k and the taper cap will be £80k. But it will take some two years to move the assessment to household basis.

2% National Insurance cut is worth up to £1,320. The changes to the non-dom regime are significant with a number of transitional provisions. Non-resident trusts will cease to be effective from 6 April 2025.

Non-doms having to revalue assets at 5 April 2019 is going to be hugely complicated and frustrating. Who will have the records to apply this in practice?

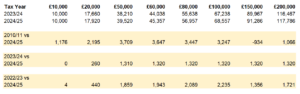

Yellow highlights show you how much you are better (or worse) off by at different earnings levels.

Robert Salter – Director, Global Mobility

The freezing of fuel duty by the Government is no surprise – Governments have not imposed any increase in fuel duty for at least the last 12 years. However, whilst expected, it does create serious question marks about the Government’s belief in the ‘green agenda’ and the legal obligation to reach ‘net zero’ by 2050.

The increase in the VAT threshold to £90,000 from £85,000 – i.e. the level of turnover at which small traders and businesses need to formally register for VAT – will certainly be welcomed by smaller businesses. However, the reality is that as the VAT threshold hadn’t changed for seven years before this announcement, there will still be a number of businesses which are caught by VAT than would have been the case based on historical norms.

The move to encourage investment in British shares via a British ISA is a questionable decision by Mr Hunt. The reality is that most advisors would suggest that a good investment strategy for savers to typically ‘spread their risk’ amongst different markets / countries and it is therefore very questionable as to whether this move will have any success.

It should also be noted that the great majority of people who invest in ISAs aren’t actually utilising their full annual ISA allowance anyway. As such, providing the opportunity for people to invest a further £5,000 in the British ISA (on top of the regular £20,000 limit) is simply going to be irrelevant to most smaller savers.

Tax changes have a long history of creating ‘unintended consequences’ from a behavioural perspective and one has to imagine that this change could be yet another example of such a case.

Abolishing the Furnished Holiday Lets regime will be a shock for those relying on those profits for the purpose of making pension contributions.

Whilst one or two aspects of Mr Hunt’s proposed changes to the non-domiciled basis of taxation should be welcome and will encourage those foreign nationals in the UK who are eligible to bring funds into the UK, a regime which only allows tax relief for four years – down from the present 15 years – is unlikely to proof popular to many international taxpayers.

In this regard, it is worth noting that many alternative regimes in other countries provide relief for 10 or 15 years (e.g. in Italy). Moreover, it is also worth noting that given the move to flexible working during Covid, it is increasingly easy for many international executives to work on a cross-border basis – that is, to live with their families in countries like Switzerland, Italy or France, whilst only spending say 2-3 days per week in the UK.

These cross-border commuters typically become ‘non-resident’ in the UK for tax purposes with the consequence that the UK tax take is restricted purely to their UK source income (e.g. the wages associated with UK workdays). Unfortunately, it is quite possible – indeed probable – that Mr Hunt’s announcement on the non-domiciled regime will simply increase the frequency of such arrangements in the coming years.

The Government’s proposed changes to the Child Benefit Clawback, meaning that for the 2024/25 tax year, it will not impact any household where no partner earns under £60,000 per annum (compared to the present £50,000 threshold) is to be welcomed.

However, whilst the Government’s move will reduce some of the unfairness that the present system creates, it certainly doesn’t eliminate the problem. As such, it would have been much fairer and simpler for the Government to recognize all the flaws of the child benefit clawback and simply remove the charge in totality.

Simon Rothenberg – Partner, Audit Accounting & Outsourcing

Fuel duty freeze will continue with UK fuel being cheaper than most of the EU, a huge change from 15 years ago.

The return on investment on the NHS is clear: Spend £4bn to save £35bn. Lots more automation is great for those that can access it – but will it work?

This is the investment in IT for the NHS which has been needed for years and indeed has been promised before. A fully integrated digital NHS will be a great thing – but I doubt that the spending will be enough and, who will design and implement the system? Hopefully not Fujitsu.

Very little in the budget for businesses – VAT threshold up and tweaking to full expensing but otherwise, no changes for businesses. This is to be welcomed as it gives a little bit of certainty for businesses in the run up to the next election when things might change much more – this should allow them to make some investment decisions in the short term at least. What businesses really want is to stop this major upheaval every few months whenever a budget happens – could we have fixed budget terms that can’t be changed?

Genevieve Morris – Head of Corporate Tax

So, there’s been a little bit for small businesses (VAT threshold increase) and a bit for mega-corps (full expensing on leased assets ‘when it’s affordable’) but where are the tax cuts and incentives for the mid-market businesses, which are the heartbeat of the UK economy?

Hunt is focused on getting people back into employment and helping businesses fill the vacancies they have. What he seems to miss is the huge cost to businesses of employing staff – employers NIC, apprenticeship levy, pension auto-enrolment, national minimum wage. Where is the employers’ NIC cut that may actually motivate more businesses to employ more people, fuelling growth and helping more people in to employment?

Well, that was certainly more sparklers than it was fireworks.

Roger Holman – Partner, Private Client

200,000 homes per year built over five years is not something to be proud of when the Government itself states that 300,000 per year are needed.

This Government seems very keen for parents to outsource parenting. No wonder so many children start primary school still not toilet trained.

Most of the users of NHS are digitally excluded. Using an app is not going to help.

John Bull – Partner, Head of US/UK Private Client

The non-domiciled tax regime is overly complex and so a more competitive alternative is welcomed, as are transitional arrangements to allow individuals to bring funds to the UK at preferential tax rates. But what about the impact on the UK Inheritance Tax (IHT) regime, which was not mentioned by the Chancellor?

Stuart Hyland – Reward Services Partner

Comparing the number of job vacancies with the number of individuals out of work is not a valid comparison and is meaningless as a justification for continued restriction of immigration. As employers across the UK economy will tell you, there are shortages in particular skill sets and we need to be encouraging and enabling schools, colleges etc to develop people with the necessary skills and resilience for the future of work. Thinking that we can plug those gaps from our current unemployed population is just disingenuous!

Heather Powell – Partner, Head of Property & Construction

Furnished Holiday Lets: So those letting their properties will now find their taxable profits are significantly higher if they have a mortgage on the property as the interest restrictions will bite, and the ability to claim capital allowances on setting up the property disappears. Combined with CGT payable increases from a possible 10% to 24%, it will be interesting to see the stats on how much tax this will raise.

Mr Hunt’s proposal to abolish the Furnished Holiday Letting Regime – the tax approach which allowed private landlords of qualifying holiday lets to get full relief for their mortgage interest payments – a relief which was not available for many long-term property rentals – was to be expected.

However, it will be interesting to see what implications this change has on the behaviour of private landlords and on the overall tourism and hospitality sector in the UK. For example, if landlords of furnished holiday lettings cease to get full tax relief for their mortgage costs, it is easy to imagine that they might try and increase the rates that they charge for the holiday lettings and hence actually make UK holidays less attractive for many tourists than those abroad.

Buy to Let landlords are leaving the market due to the complexity of complying with the ever-increasing legislation, and the restriction on the quantum of mortgage interest that can be deducted when calculating rental profits. The reduction in the CGT rate to 24% may trigger further sales – especially if landlords fear Labour will reverse this change.

Unintended consequences – the businesses supplying those on holiday in the UK are going to have a look at their business model – and start considering if they should change the focus on serving the local population. However, it is inevitable that if holiday lets are sold or let to locals the money spent in a local area will reduce… some of our coastal regions are totally dependent on spending by holidaymakers. Investment is needed to revitalise these regions and encourage new businesses to flourish.

Kohtaro Hirota – Head of Japan Desk

The British ISA is good news for retail investors, as on top of this £25K new threshold, they can enjoy the current annual exemption for capital gain and dividend allowance by having another investment account which is not ISA.

Abolishment of non-dom regime: Japanese employers in the UK need to carefully plan the length of the UK assignment for their Japanese assignees seconded from Japan.

Further NIC cut: No impact for Certificate of Coverage (COC) covered Japanese assignees unless they stay in the UK for more than eight years.

Nick Winters – Head of Technology

Microsoft and Google, among others, have invested heavily in the UK. The Chancellor remains supportive of Tech and other high growth industries, announcing new measures to support them. This consistent support is welcomed. It helps to continue to attract significant international investment in the UK and to reward UK based high growth businesses so that they grow here and remain here.

Stefanie Tremain – Partner, Private Client

Also ‘abolish’ sounds straightforward, but the last major change to property tax led to several years of complex transitional rules.

The policy document states that for offshore trusts, income and gains will be taxed on the settlor on an arising basis after four years, so we are back to pre-2017 rules, with grandfathering for pre-April 2025 income and gains. Looks like IHT protection continues for trusts set up pre-April 2025… the offshore trust merry go round continues.

Simon Sutcliffe – Customs and Excise Duty Partner

Vaping: Instead of banning we tax! Surely, in light of health concerns amongst younger users of vaping products we should be looking at removing these products from the marketplace as they have limited smoking cessation benefits. Additionally, introducing the excise levy in 2026 is too far in the future.

Fiona Fernie – Partner, Private Client

The announcement that the Chancellor is going to resource HMRC to collect the proper tax due is long overdue but what does it mean, where is the money coming from and how will he allocate it?

Will there be guidance from the Government as to how it should be spent e.g. staff training, online assistance and AI.

The abolishment of the non-dom regime will (after the transitional period) simplify the tax system for non-UK nationals coming to the UK which is obviously welcome. However, the four-year period of ‘exemption’ may be significantly short that those that we want to attract to the UK do not become integrated into UK life to a point which prevents them leaving as soon as the exemption period is over.

Winnie Cao – Partner, Head of China Desk

Typically, new migrants to the UK are required to reside five years before they acquire Indefinite Leave to Remain, subsequently naturalisation. While we need more details on the replacement scheme for non-dom regime, it will mean that those highly desirable migrants with skills, talents, and wealth, will need to think twice before they land in the UK in the fear that they may need to potentially pay worldwide tax in year five before acquiring Indefinite Leave to Remain.

As the Chancellor says, the key attraction of the UK is its education, tech and science sector. All these sectors require new migrants to spend a substantial time in the UK, whether they are here for education, investing in new tech start-ups, and/or research in life science projects – much more beyond a four-year period as indicated by the new replacement scheme. In the ever-increasing talent war and attraction for investment into the UK, we need to think about the potential damage that the replacement scheme will cause for new migrants comparing the UK with other jurisdictions.

Sean Randall – Stamp Duty Partner

The Government has chosen to abolish a Stamp Duty Relief that incentivises investment in the public rented sector (PRS). The relief can reduce the Stamp Duty Rate for relevant purchases to as low as 1%. Although the relief has undoubtedly helped investment in the PRS, it has also encouraged claims being made in respect of family homes with annexes – worth up to £88,750 of tax relief for a single annexe. The extent to which the relief was (and continues to be) claimed on annexes has probably driven the decision to abolish it altogether. The Stamp Duty reclaim farms that have built their business around this activity will need to switch to something else. Property companies and institutional investors in PRS will surely be angry that the Government has ‘thrown the baby out with the bathwater’ rather than tackling abuse or unfairness head on.

Paul Haywood-Schiefer – Senior Manager Private Client

The Chancellor’s reforms on non-doms are welcome but what will the uptake be here. Most non-doms have the ability to move country and manage their time in the UK to be non-resident. Furthermore, when it comes to actual tax benefits from the regime, many are more worried about IHT in the UK than income and CGT rates. Therefore, with no change there, will we see a significant number leave the UK before the new rules come into effect, tempering the £15bn expected to be raised?

John Havard – Consultant, US UK Private Client

Transitional rule: Existing non-doms already in the UK at the change date, but who have been here for less than four years, will get the new relief until the end of their fourth year of tax residence.

From April 2025 new arrivals who have had a period of at least 10 years non-residence pre-arrival will be exempt from UK tax on overseas income gains for the first four years in the UK.

Andrew Sanford – Partner, Audit Accounting & Outsourcing

The biggest issue affecting public finances is an ageing population and declining birth rate. It’s disappointing that the Government never mention this. It appears far too difficult to resolve.

The spending commitments on levelling up are dwarfed by the £3 billion of unspent funds in the apprentice levy pot that are now time expired.

Nothing on income tax thresholds – more tax has been collected through inflation putting tax-payers into higher tax bands than any national insurance cuts.

Alan Pearce – Partner, Corporate Tax

This is less than a 6% increase and doesn’t make up for the years when this threshold was not increased.

Would you like to know more?

If you have any questions about the Government’s Spring Budget and how it may impact you, please get in touch with your usual Blick Rothenberg contact or John Bull or Genevieve Morris using the details on this page. For any media enquiries, please contact David Barzilay.

You can also visit our Budget Hub, where you can find our commentary and a range of insights to help you better understand how the Budget may affect you.

Contact Us

You may also be interested in

Spring Budget 2024: Analysis

Spring Budget 2024: Winners and Losers