Beneficial Ownership Information Reporting

New reporting requirements regarding Beneficial Ownership Information take effect from 1 January 2024

New reporting requirements, which take effect from 1 January 2024, require most US corporations and limited liability companies, as well as most non-US entities that are registered to do business in the US, to report information about their beneficial owners to the US Treasury Financial Crimes Enforcement Network (FinCEN).

While UK businesses are accustomed to reporting details of shareholders and beneficial owners to HM Revenue & Customs (HMRC), these reporting requirements are new for the majority of US businesses.

The purpose of this reporting is to unmask shell companies used for money laundering, drug trafficking and other criminal activity, but it will impact a large number of US-connected businesses.

Who must file? Reporting companies

All ’reporting companies’ will be required to report their beneficial ownership information. However, the definition of a reporting company differs for US domestic entities and foreign entities.

A domestic reporting company is defined as

- a corporation

- a limited liability company, or

- any other entity created by the filing of a document with a secretary of state or any similar office under the law of a state or Indian tribe.

A foreign reporting company is any entity that is:

- a corporation, limited liability company, or other entity formed under the law of a foreign country, and

- registered to do business in any US state or in any tribal jurisdiction, by the filing of a document with a secretary of state or any similar office under the law of a U.S. state or Indian tribe.

Exceptions from filing

There are 23 types of entities which are exempt from the beneficial ownership information reporting requirement. However, the large majority of these are subject to federal or state regulation and beneficial ownership reporting requirements. There are no exemptions for small businesses which makes this filing obligation particularly burdensome.

The exempt entities are listed below. However, it is worth noting that an entity must meet specific criteria to qualify for an exemption. It is our expectation that almost all businesses will need to file.

Exempt entities

Certain types of securities reporting issuers

- A US governmental authority

- Certain types of banks

- Federal or state credit unions as defined in section 101 of the Federal Credit Union Act

- Bank holding company as defined in section 2 of the Bank Holding Company Act of 1956, or any savings and loan holding company as defined in section 10(a) of the Homeowners’ Loan Act

- Certain types of money transmitting or money services businesses

- Any broker or dealer, as defined in section 3 of the Securities Exchange Act of 1934, that is registered under section 15 of that Act (15 U.S.C. 78o)

- Securities exchanges or clearing agencies as defined in section 3 of the Securities Exchange Act of 1934, and that is registered under sections 6 or 17A of that Act

- Certain other types of entities registered with the Securities and Exchange Commission under the Securities Exchange Act of 1934

- Certain types of investment companies as defined in section 3 of the Investment Company Act of 1940, or investment advisers as defined in section 202 of the Investment Advisers Act of 1940

- Certain types of venture capital fund advisers

- Insurance companies defined in section 2 of the Investment Company Act of 1940

- State-licensed insurance producers with an operating presence at a physical office within the United States, and authorised by a state, and subject to supervision by a state’s insurance commissioner or a similar official or agency

- Commodity Exchange Act registered entities

- Any public accounting firm registered in accordance with section 102 of the Sarbanes-Oxley Act of 2002

- Certain types of regulated public utilities

- Any financial market utility designated by the Financial Stability Oversight Council under section 804 of the Payment, Clearing, and Settlement Supervision Act of 2010

- Certain pooled investment vehicles

- Certain types of tax-exempt entities

- Entities assisting a tax-exempt entity

- Large operating companies with more than 20 full-time employees, more than $5,000,000 in gross receipts or sales, and an operating presence at a physical office within the US

- The subsidiaries of certain exempt entities

- Certain types of inactive entities that were in existence on or before 1 January 2020, the date the Corporate Transparency Act was enacted.

What must be reported?

FinCEN will collect identifying information about the individuals who directly or indirectly own or control an entity through this filing. However, unhelpfully to date, no draft of the form has been released.

The beneficial owners name, date of birth, and address will need to be reported, along with a unique identifying number from an acceptable identification document, along with an image of the identification document.

Acceptable identification documents include:

- A non-expired driver’s license issued by a US state

- A non-expired identification document issued by a US state or local government, or Indian Tribe that is issued for the purpose of identifying the individual

- A non-expired passport issued by the US Government

- If the individual does not have any of the three forms of identification document described above, the reporting company may provide the identifying number from a non-expired passport issued by a foreign government.

In addition to details of the beneficial owner, we know that reportable companies created prior to 1 January 2024, will need to report information about itself, including its legal and trading names, address, and taxpayer identification number.

Who is a reportable beneficial owner?

Generally, a beneficial owner is an individual who directly, or indirectly holds substantial control over the reporting company or directly or indirectly owns or controls 25% or more of the ownership interest of the entity.

Substantial control can include the power to control important decisions the entity makes, or the position of a senior officer of the entity.

Ownership interests include simple shareholdings as well as more complex ownership structures and agreements.

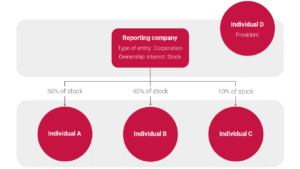

The following illustrative example is provided by FinCEN:

Example 2: The reporting company is a corporation. The company’s total outstanding ownership interests are shares of stock. Three people (individuals A, B, and C) own 50 percent, 40 percent, and 10 percent of the stock, respectively, and one other person (individual D) acts as the President for the company but does not own any stock.

Assuming there are no other facts, individuals A, B, and D are all beneficial owners of the company and their information must be reported. Individual C is not a beneficial owner.

- Individual A owns 50 percent of the company’s stock and therefore is a beneficial owner because they own 25 percent or more of the company’s ownership interests.

- Individual B owns 40 percent of the company’s stock and therefore is a beneficial owner because they own 25 percent or more of the company’s ownership interests.

- Individual C is not a company officer and does not directly or indirectly exercise any substantial control over the company.

- Individual C also owns 10 percent of the company’s stock, which is less than the 25 percent or greater interest needed to qualify as a beneficial owner by virtue of ownership interests. Individual C is therefore not a beneficial owner of the company.

- Individual D is president of the company and is therefore a beneficial owner. As a senior officer of the company, individual D exercises substantial control, regardless of whether the individual owns or controls 25 percent or more of the company’s ownership interests.

When must the filing be submitted?

Reporting companies created or registered to do business in the US prior to 1 January 2024 must submit their initial Beneficial Ownership Information report by 1 January 2025.

Reporting companies created or registered to do business in the US on or after 1 January 2024, but before 1 January 2025 must submit their initial Beneficial Ownership Information report within 90 days of creation or registration.

Reporting companies created or registered to do business in the US on or after 1 January 2025 must submit their initial Beneficial Ownership Information report within 30 days of creation or registration.

Updated reports must be submitted when there is a change to the previously reported information about the company or its beneficial owners and must be submitted within 30 days of the change.

What should transatlantic businesses do?

It is highly likely that a UK business that has expanded into the US will be subject to this reporting requirement.

UK businesses engaged in a US trade or business are likely required to report information about the UK business and its beneficial owners, while UK businesses who have incorporated a US subsidiary will be required to report information about the subsidiary as well as the ultimate beneficial owners.

Additional information

Beneficial Ownership Information Reporting | FinCEN.gov

BOI Reporting Key Questions (fincen.gov)

Video from U.S. Department of the Treasury

Would you like to know more?

If you would like to discuss how the above may affect you, please get in touch with your usual Blick Rothenberg contact, or Michael Holland using the form below.

Contact Michael

You may also be interested in

Another bumper tax take for HMRC

Americans who sell homes they have purchased in the UK could still face a hefty tax bill