R&D claims – Mandatory notification forms

Ele Theochari discusses the new claim notification form that is coming into effect for accounting periods beginning on or after 1 April 2023

Ele Theochari discusses the new claim notification form that is coming into effect for accounting periods beginning on or after 1 April 2023 that many businesses may not be aware of.

Why is it relevant?

For accounting periods beginning on or after 1 April 2023, companies may need to submit an ‘Advanced Notification Form’ to HMRC within six months of the year end. Broadly, this form will require basic details about the company (e.g. Unique Taxpayer Reference, VAT number, PAYE reference) and:

“a summary of the high-level planned activities, for example if you’ve developed software, what it will be used for to show that the project meets the standard definition of R&D”.

Although the R&D tax relief regime allows companies to make R&D claims for the previous two accounting periods, the aim of this form is to curtail last-minute claims where R&D has been ‘found’ by unscrupulous advisers.

Who does it affect?

The Advanced Notification Form applies to R&D claims made under both the SME and large company (Research and Development Expenditure Credit or RDEC) schemes and will continue to be relevant under the merged scheme. It is required if:

- the company is claiming R&D relief for the first time, or

- the company has not made an R&D claim in the past three years.

As an illustrative example, for the 12 months ended 31 March 2024 the claim notification deadline will be 30 September 2024. If the company has made an R&D claim at any time during the three-year period between 1 October 2021 – 30 September 2024 and the claim was not made by amending the tax return on or after 1 April 2023, a notification form will not be required. It is important to note, however, that when making this assessment a company must consider the date an R&D claim was made. For example, if a company submits a tax return including an R&D claim (for the first time) for the year ended 31 March 2023 in October 2024, a notification form will still be required for the year ended 31 March 2024.

It is also important to consider if previous claims in the past three years were made by amending the tax return after its initial submission or not. If the claim was made by amending a tax return after its initial submission, and the amendment was received on or after 1 April 2023, a notification form will be required.

What do you need to know?

With the first 12-month period approaching on 31 March 2024, many businesses will need to consider whether this form will be required and make the necessary submission no later than 30 September 2024. This will be earlier for short accounting periods that began on or after 1 April 2023.

For long accounting periods, only one notification form will be required, and the notification deadline will remain six months after the end of the long accounting period, rather than being split into 12 months and the remainder.

HMRC have confirmed that an R&D claim will be removed from a tax return as an ‘error’ where the form was required but not submitted, and that little recourse will be available where a company is outside of the claim notification window.

The ‘Advanced Notification Form’ is submitted online, following the same process as the Additional Information Form. Further information can be found on the Government website here.

What should you do next?

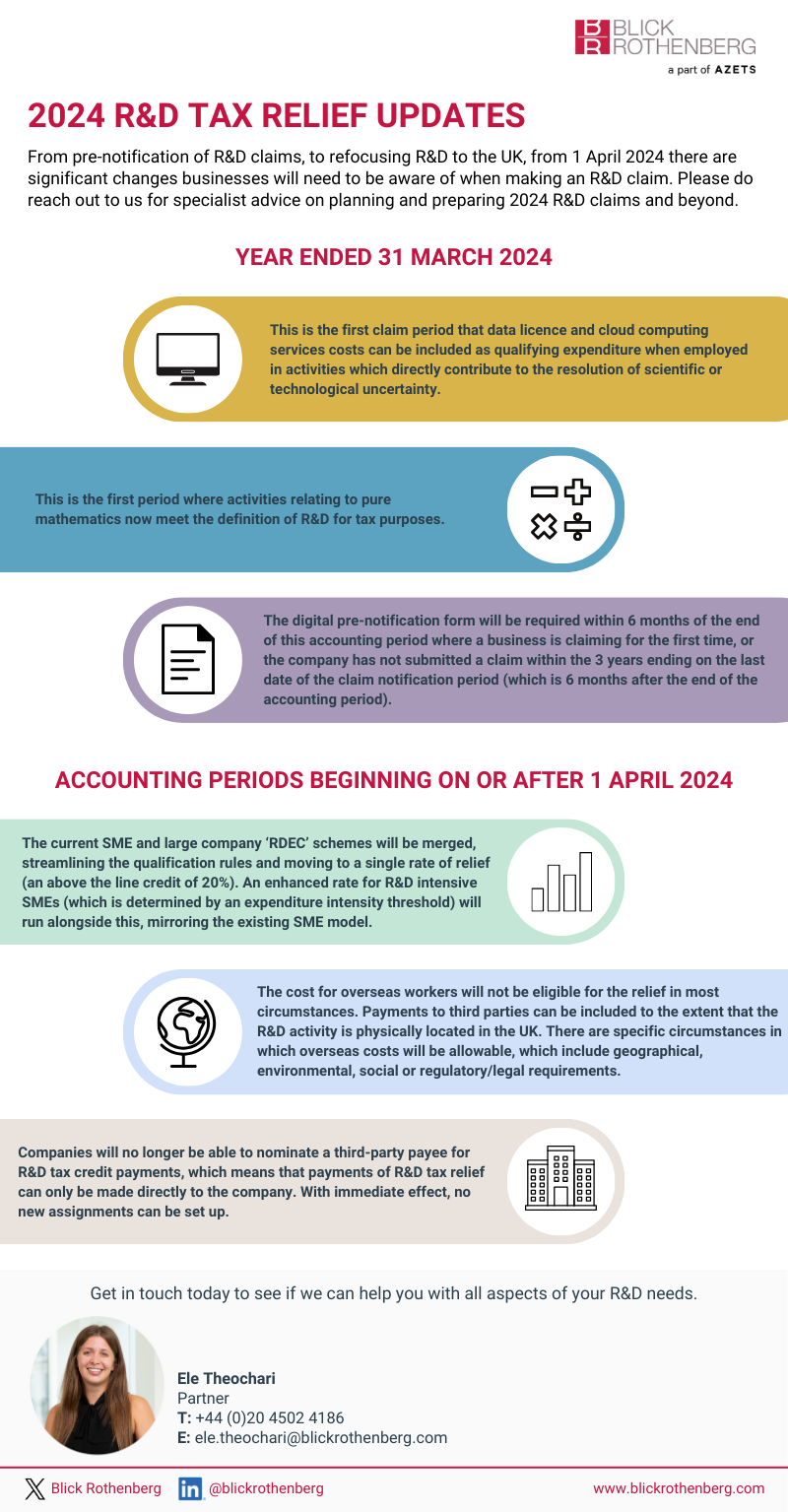

You can also take a look at our infographic that outlines the R&D tax relief updates and the significant changes from 1 April 2024 that businesses need to be aware of.

{kind=link}

If you are in any doubt as to the implications of the above, please reach out to us to see how this may affect your upcoming R&D claims.

Contact us

If you would like to discuss the above matter, or to confirm how this impacts your company, please get in touch with your usual Blick Rothenberg contact, or Ele Theochari using the form below.

Contact Ele

More Spotlight on… articles

Spotlight on… Changing Accounting Standards – The biggest shake-up to UKGAAP in a decade

The Economic Crime and Corporate Transparency Act 2023 -ECCTA